Short-Termism

Posted:October 13, 2015

Categories:

Paul Hancock, CFP® October 13, 2015

What does Vanguard’s CEO, a portfolio manager, and an economist have in common? They all agree investors focus way too much on the short-term.

“Looking at investments in less than a 5 to 10 year window is time wasted. People should be thinking in 10-year increments around their portfolios because it’s really difficult to have any sense in the short-run what is going to happen.” Bill McNabb, Vanguard’s CEO

Short-termism refers to an excessive focus on short-term results at the expense of long-term interests. How do you define “short-term” in investing? My argument has always been that any money you intend to use in the next 5 years has no business being invested in the stock market. Examples include your emergency fund or savings towards a one-time expense such as a car or a house. At today’s low interest rates, you give up return for preservation of capital. However, you know with confidence that cash will be available when needed. Many investors now have the bulk of their savings in retirement accounts (IRA, 401k, and 403b). The beauty of these accounts is that their natural time horizons are very long-term in nature. Consider the 22-year old entering the work force who plans to retire at age 65. The “built-in” time horizon for his 401(k) is 43 years to retirement plus likely another 25-30 years during retirement. For a 22-year old, that’s a 70-year time horizon!

How about retirees or those close to retirement? Naturally, time horizons are shorter and strategies shift from wealth accumulation to distribution. This stage of life requires specific planning that helps investors stay focused on the long-term during retirement. Consider how much income you’ll need to meet a reasonable budget in retirement. Determine your sources of income outside of your portfolio such as part-time work, social security, and pension income. Finally, determine the amount of cash flow you’ll need from your portfolio to supplement your other sources of income. This exercise will help you develop an appropriate asset allocation (stocks vs. bonds) during retirement to fund your income needs. Although stocks are riskier assets than bonds and cash, you should not abandon stocks during retirement as they’ll help balance a portfolio, provide protection against inflation and have historically produced higher returns than bonds over a long periods of time.

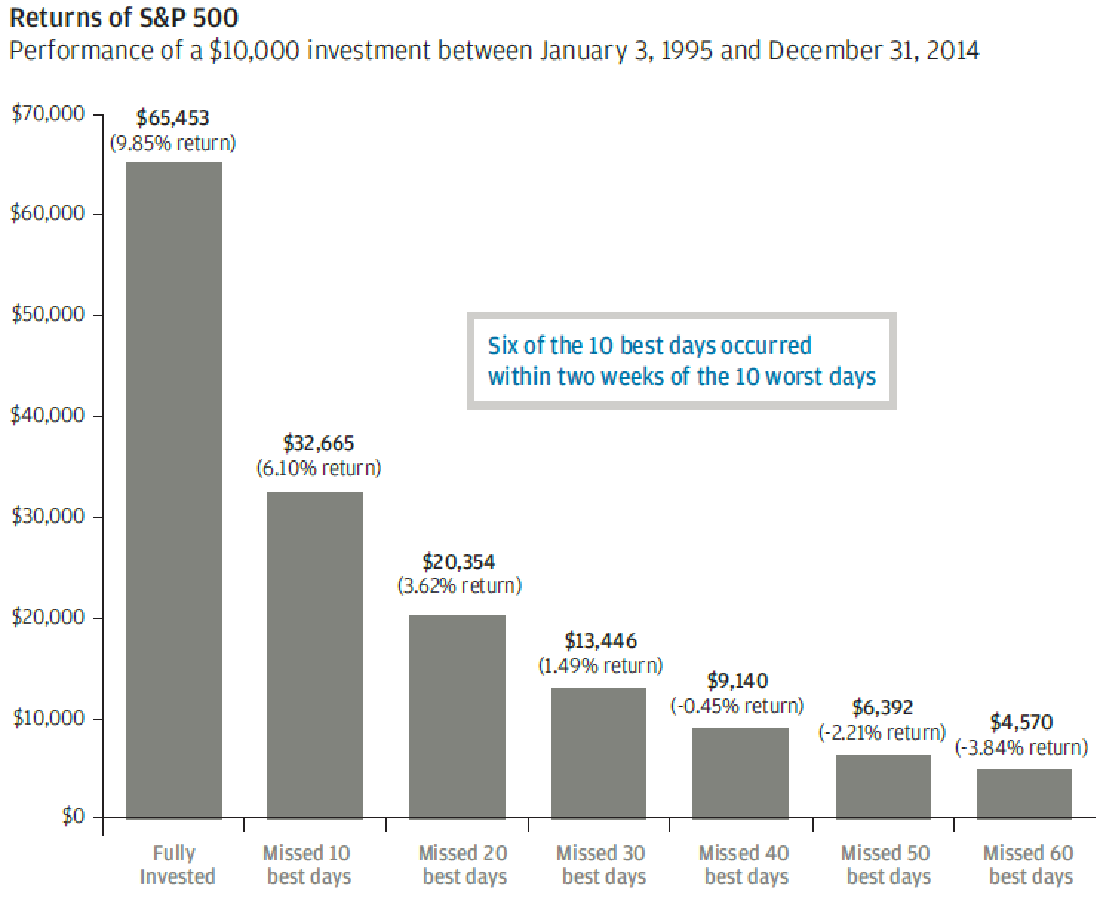

A common investment strategy associated with short-termism is market timing; the strategy of making buy or sell decisions of financial assets (often stocks) by attempting to predict future market price movements. Market timers often buy and sell many times during the day and rarely are fully invested at all times. Consider the following example (see chart below):

- A 20-year investment in the S&P 500 Index between 1/3/1995 to 12/31/2014 produced an annualized return of 9.85%.

- If you engaged in market timing during this same time period and missed the 10 best days, your return dropped to 6.10%. For comparison, bonds returned 6.21% over that time period.

- Your return goes negative if you missed the 40 (out of 7,300) best days during this time period.

- Six of the 10 best days occurred within two weeks of the 10 worst days which can often be a time when investors are not fully invested.

Granted, investing is rarely is this “easy,” but this is a great reminder to stay committed to a long-term strategy and portfolio asset allocation.

Source: JP Morgan

It seems that patience is becoming less of a virtue in today’s society. Consider some examples of short-termism:

- The average CEO tenure has decreased from about 10 years to about 5½ years since the 1990s.

- In a recent series of surveys of executives at large US firms, around 90% of managers reported pressure to meet earnings targets. Almost half of executives reported that they would reject a profitable project if taking the project meant missing short-term profit targets.

- The average tenure of a college football coach is now only 4 years, much like the experience of most college students themselves!

- Portfolio turnover has increased from 30% in the 1960s to 140% today. That means in the 60s portfolio managers would hold their stocks for roughly 3 years. Today, the hold time is much less as fund managers buy and sell their entire portfolio in less than a year on average.

- Household savings rates have dropped from 11.2% in 1959 to 4.6% today.

It’s important to understand how your portfolio is invested in order to align your objectives to meet a desired goal. Also, tracking performance is necessary in order to evaluate your progress towards achieving your goals. However, getting carried away with short-term movements in markets can de-rail a long-term plan. A more prudent course of action is to invest towards a defined goal, save consistently and maintain a long-term perspective.

Stocks fell sharply in the third quarter with emerging markets falling the most. Concerns over growth in China, falling commodity prices, a strong US dollar, and weak global growth increased volatility. A “phantom” interest rate hike from the Federal Reserve added to volatility as the global economy begins to adjust to tighter monetary policy from the United States. When the Fed actually hikes rates is anyone’s guess. What’s becoming evident is that the Fed has a tough task ahead as they begin to tighten amidst a slowing and much more volatile global economy.

The bond market posted mostly positive results with higher risk parts of the bond market like high yield declining in the quarter commensurate with other risk assets. The US dollar continues to strengthen, hurting commodities and those economies driven by commodity-based consumption.

A balanced portfolio of 60% stocks and 40% bonds has declined 5.2% during the quarter, but still has posted positive returns over the past 3, 5 and 10 year periods.

References

Masters in Business Podcast – An Interview with Bill McNabb. May 15, 2015. Available online at Bloomberg.com

Financial Times – Definition of short-termism. Available online at lexicon.ft.com

JP Morgan Guide to Retirement 2015 Edition. Available online at jpmorganfunds.com

The American CEO.com

A Wealth of Common Sense – Ben Carlson

St. Louis Federal Reserve FRED Economic Data – Personal Savings Rate Data. Available online at research.stlouisfed.org

DISCLOSURES & INDEX DESCRIPTIONS

All indexes are unmanaged and an individual cannot invest directly in an index. Index returns do not reflect fees or expenses.

The MSCI ACWI (All Country World Index) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. As of June 2009 the MSCI ACWI consisted of 45 country indices comprising 23 developed and 22 emerging market country indices.

The S&P 500 Index is widely regarded as the best single gauge of the U.S. equities market. This world-renowned index includes a representative sample of 500 leading companies in leading industries of the U.S. economy. Although the S&P 500 Index focuses on the large-cap segment of the market, with approximately 75% coverage of U.S. equities, it is also an ideal proxy for the total market. An investor cannot invest directly in an index.

The Russell 3000 Index® measures the performance of the 3,000 largest U.S. companies based on total market capitalization.

The Russell Midcap Index ® measures the performance of the 800 smallest companies in the Russell 1000 Index.

The Russell 2000 Index ® measures the performance of the 2,000 smallest companies in the Russell 3000 Index.

The MSCI® EAFE (Europe, Australia, Far East) Net Index is recognized as the pre-eminent benchmark in the United States to measure international equity performance. It comprises 21 MSCI country indexes, representing the developed markets outside of North America.

The MSCI Emerging Markets Index SM is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. As of June 2007, the MSCI Emerging Markets Index consisted of the following 25 emerging market country indices: Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Israel, Jordan, Korea, Malaysia, Mexico, Morocco, Pakistan, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

The Dow Jones Composite REIT Index measures the performance of Real Estate Investment Trusts (REIT) and other companies that invest directly or indirectly through development, management or ownership, including properties.

The Dow Jones-UBS Commodity Index is composed of futures contracts on physical commodities and represents twenty two separate commodities traded on U.S. exchanges, with the exception of aluminum, nickel, and zinc.

The Barclays Capital U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indexes that are calculated and reported on a regular basis.

The Barclays U.S. Treasury Index is U.S. Treasury component of the U.S. Government index. Public obligations of the U.S. Treasury with a remaining maturity of one year or more.

Treasury bills are excluded (because of the maturity constraint). Certain special issues, such as flower bonds, targeted investor notes (TINs), and state and local government series (SLGs) bonds are excluded. Coupon issues that have been stripped are reflected in the index based on the underlying coupon issue rather than in stripped form. Thus STRIPS are excluded from the index because their inclusion would result in double counting. However, for investors with significant holdings of STRIPS, customized benchmarks are available that include STRIPS and a corresponding decreased weighting of coupon issues. Treasuries not included in the Aggregate Index, such as bills, coupons, and bellwethers, can be found in the index group Other Government on the Index Map. As of December 31, 1997, Treasury Inflation-Protection Securities (Tips) have been removed from the Aggregate Index. The Tips index is now a component of the Global Real index group.

The Barclays Short Treasury Index includes aged U.S. Treasury bills, notes and bonds with a remaining maturity from 1 up to (but not including) 12 months. It excludes zero coupon strips.

The Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term tax-exempt bond market. To be included in the index, bonds must be rated investment-grade (Baa3/BBB- or higher) by at least two of the following ratings agencies: Moody's, S&P, Fitch. If only two of the three agencies rate the security, the lower rating is used to determine index eligibility. If only one of the three agencies rates a security, the rating must be investment-grade. They must have an outstanding par value of at least $7 million and be issued as part of a transaction of at least $75 million. The bonds must be fixed rate, have a dated-date after December 31, 1990, and must be at least one year from their maturity date. Remarketed issues, taxable municipal bonds, bonds with floating rates, and derivatives, are excluded from the benchmark.

The Barclays U.S. Corporate Investment Grade Index is the Corporate component of the U.S. Credit index. Publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered.

The Barclays U.S. Corporate High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included. Original issue zeroes, step-up coupon structures, 144-As and pay-in-kind bonds (PIKs, as of October 1, 2009) are also included.

The Barclays Global Aggregate Bond Index provides a broad-based measure of the global investment-grade fixed income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indices. The index also includes Eurodollar and Euro-Yen corporate bonds, Canadian government, agency and corporate securities, and USD investment grade 144A securities.

The Barclays Emerging Markets USD Aggregate Index is a flagship hard currency Emerging Markets debt benchmark that includes USD denominated debt from sovereign, quasi-sovereign, and corporate EM issuers. The index is broad-based in its coverage by sector and by country, and reflects the evolution of EM benchmarking from traditional sovereign bond indices to Aggregate-style benchmarks that are more representative of the EM investment choice set. Country eligibility and classification as an Emerging Market is rules-based and reviewed on an annual basis using World Bank income group and International Monetary Fund (IMF) country classifications. This index was previously called the Barclays US EM Index and history is available back to 1993.

Index Date Sources: MSCI, Russell, Standard & Poors, Morningstar, Kwanti, Barclays, Hatteras

The chart referenced in the article was taken from JP Morgan. The chart is for illustrative purposes only and does not represent the performance of any investment or group of investments. Source: Prepared by J.P. Morgan Asset Management using data from Lipper. 20-year annualized returns are based on the S&P 500 Total Return Index, an unmanaged, capitalization-weighted index that measures the performance of 500 large capitalization domestic stocks representing all major industries. Past performance is not indicative of future returns. An individual cannot invest directly in an index. Data as of December 31, 2014.

Past performance is no guarantee of future results. Diversification does not assure profit or protect against a loss in a declining market. While we have gathered this information from sources believe to be reliable, we cannot guarantee the accuracy of the information provided. The views, opinions, and forecasts expressed in this commentary are as of the date indicated, are subject to change at any time, are not a guarantee of future results, do not represent or offer of any particular security, strategy, or investment and should not be considered investment advice. Investors should consider the investment objectives, risks, and expenses of a mutual fund or exchanged traded fund carefully before investing. Furthermore, the investor should make an independent assessment of the legal, regulatory, tax, credit, and accounting and determine, together with their own professional advisers if any of the investments mentioned herein are suitable to their personal goals.

International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Small and mid-cap stocks carry greater risks than investments in larger, more established companies. Fixed-income securities are subject to interest-rate risk. Investing in high-income securities may carry a greater risk of nonpayment of interest or principal than higher-rated bonds. Investing in commodities is generally considered speculative because of the significant potential for investment loss due to cyclical economic conditions, sudden political events, and adverse international monetary policies. There are several risks associated with alternative or non-traditional investments above and beyond the typical risks associated with traditional investments including higher fees, more complex/less transparent investment strategies, less liquid investments and potentially less tax-friendly. Some strategies may disappoint in strong up markets and may not diversify risk in extreme down markets.

To receive a copy of Genesis Wealth Planning’s ADV Part II which contains additional disclosures, proxy voting policies and privacy policy, please contact us.