Hurricanes, Tornadoes & Hyperinflation

Posted:October 17, 2024

Categories: Inflation, Fiat Currency, Stock Market

During my lifetime, I’ve primarily lived in Iowa and Florida. Both have very different climates and weather conditions. As Hurricane Milton approached the West Coast of Florida on October 9th, it felt like I was back in the Midwest. Numerous tornado warnings were issued during the day as the “outer bands” of Milton came ashore in Southern Florida. Our thoughts and prayers are with those directly affected by this storm and Hurricane Helene. It’s been an active hurricane season.

“You Iowa folk can relate to these tornados- I don't like these.”

This text came across my phone in a group text of a few families from our church. It was early in the afternoon on the 9th as we were finishing our hurricane prep. Hurricane Milton was unique as it developed in the western Gulf of Mexico and then traveled towards Florida. As the hurricane approached, the winds moved counterclockwise around the eye of the storm. The “bands” were also coming counterclockwise pushing storms in from the southern part of Florida. High in the atmosphere, strong upper-level winds pushed dry air clockwise which then “collided” with the bands. This collision effect is what causes tornadoes to spin up and form. According to reports, there were 130+ tornado warnings issued in Florida on October 9th, the second most of all time in a single state in the history of the United States. See Figure 1 for a visible representation of this.

These tornadoes that ripped through the state included an EF-3 and one that lasted 140 minutes.

“Fort Pierce & Spanish Lakes, FL, tornado, was rated an EF-3, with maximum sustained winds of 155 MPH. The tornado was on the ground for 13 miles.” Via X @MaxVelocityWX

“A 140 MINUTE TORNADO was confirmed from Hurricane Milton, starting at 9:42am, and ending at 12:02pm, as an EF-1 tornado. This tornado started in Collier County and ended in Glades County.” Via X @MaxVelocityWX

Having lived through three major hurricanes in seven years, I can tell you they are not fun. They are more like an emotional rollercoaster. The striking difference between hurricanes and tornadoes is time. With a hurricane, you generally have at least a week to prepare. A tornado can form at any moment.

Figure 1: Hurricane Milton Tornado Warnings in Florida

Source: Via X @PettusWX

Hyperinflation

Both hurricanes and tornadoes remind me of hyperinflation.

There are varying definitions of hyperinflation. The “non-monetary” economist defines hyperinflation as a large “cost-push” inflation where rising oil prices or rising demand cause inflation and then hyperinflation. The “monetary” economists define inflation as an abnormal rise in the money supply. Said another way, hyperinflation is caused by an abnormal excess amount of money printed by central banks to finance government deficits. The most famous proponent of the monetarist view, Milton Friedman once quipped “Inflation is always and everywhere a monetary phenomenon”.

Another way to view hyperinflation is to say it’s very high inflation levels. This can be monetary inflation or “high street” price inflation which is more commonly quoted in the financial media. Hyperinflation as it relates to price inflation is widely believed to occur when the monthly increase of inflation is more than 50 percent.

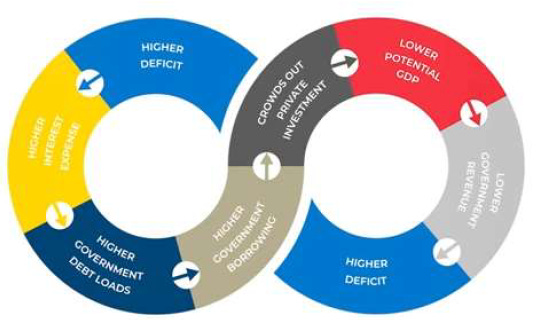

Hyperinflation doesn’t happen all at once. Much like a hurricane, it builds and builds over time as the money supply and debt increase. Those paying attention can see it coming. At a certain point, too much money and debt are accumulated which causes a negative feedback loop. That “breaking point” also reminds me of tornadoes, such as what Germany experienced in 1923 after World War I. See figure 2 below. What can occur is as follows:

Higher government debt loads lead to → Higher government borrowing → Crowding out private investment → Translates into lower potential GDP growth → Causes government revenue (taxes) to fall → Creating a higher deficit → Leading to higher interest expenses → Feeding back into more government debt loads.

Figure 2: Government Debt Negative Feedback Loop

Source: DoubleLine Capital

To say hyperinflation is only caused by an abuse of the money printer is just too simplistic according to James Montier. If this were true, there would be many more historical examples of hyperinflation. In a 2013 white paper, he looked back at several historical samples of hyperinflation and found some common characteristics. These characteristics help bridge the gap between the “non-monetarist” view and the “monetarist view.”

- Large Supply Shocks. “Often, but not always, wars of one form or another cause large supply shocks. Regime change is also often seen as a cause. The role of supply shocks is critical in the creation of hyperinflations. They represent a hit to potential output and thus are a key mechanism for creating the excess demand so often seen during hyperinflations.” (Montier, 2013)

A more recent example of a global “supply shock” was what we experienced during COVID. Combine the supply shock with money printing, this created the large price inflation in 2021 to today. This also happened with oil prices in the 1970s which was a large input to rising inflation during that decade.

- Big debts denominated in a foreign currency. “This practice leads to the devaluation of the currency, which in turn leads to the rising price level.” (Montier, 2013)

The Asian financial crisis of the late 1990s was mostly due to nations borrowing too much money in the Eurodollar system. When the exchange rates got out of control for these emerging markets, they had no choice but to devalue their currencies.

- Distributive conflict/transmission mechanism. “Crucially, the need for this element was pointed out by Joan Robinson in 1938. She wrote “Neither exchange depreciation nor a budget deficit can account for inflation by itself. But if the rise in money wages is brought into the story, the part which each plays can be clearly seen. With the collapse of the mark in 1921, import prices rose abruptly, dragging home prices after them. The sudden rise in cost of living led to urgent demands for higher wages. Unemployment was low . . . profits were rising with prices, and the German workers were faced with starvation. Wage rises had to be granted. Rising wages, increasing both home costs and home money incomes, counteracted the effect of exchange depreciation in stimulating exports and restricting imports. Each rise in wages, therefore, precipitated a further fall in the exchange rate, and each fall in the exchange rate called forth a further rise in wages. This process became automatic when wages began to be paid on a cost-of-living basis.” (Montier, 2013)

The above described what happened in Germany during the Weimar Republic hyperinflation in 1922-1923 following World War I. Germany had a large amount of war reparation debt owed to France, the UK, and the U.S. which was to be paid in gold. Gold was used as money/currency during this time and thus they had a large debt owed in a foreign currency. Unfortunately, you can’t print gold bars. Furthermore, Germany could not export goods to earn revenue in gold to pay their debt obligations. The goods produced were immediately consumed by their citizens. A crazy chart shows the price of gold in their local currency that eventually hyperinflated, the Mark.

Figure 3: Gold Price in Weimar Marks

Source: Via X @Myrmikan

United States & Hyperinflation

The last time the United States faced a government debt-to-GDP ratio well above 100% was after World War II. From roughly 1945 to 1965, we were able to work off this debt load by keeping government bond interest rates low and GDP high (figure 4). The 10-year U.S. treasury average was just above 3% during this period, while GDP averaged 6%. Thus, our government debt to GDP went from 106% in 1946 to 37% in 1965. Keep in mind, that inflation was also kept above interest rates, thereby providing investors in bonds a negative real return.

Figure 4: Federal Debt & 10-Year U.S. Treasury

Source: DoubleLine Capital

A natural question is will the United States and the dollar ultimately hyperinflate? Although I will never say no with 100% certainty, I believe the chance of hyperinflation in the dollar is highly unlikely. The dollar remains the global reserve currency. There is an incredibly large demand for dollars. We do not owe a large amount of money in a foreign currency as we can print dollars. We also own a large amount of gold in reserve, the most of any country on the planet. Supply shocks and wars are certainly a risk, but completely out of our control. Fiscal restraint is also a path out of this debt trap. The U.S. is home to a large number of well-run companies with global footprints. Finally, the U.S. Treasury and Federal Reserve have several levers to pull to prevent interest rates from spiraling out of control. However, my view is that interest rates will remain elevated leading to higher price inflation in the coming years. But a hyperinflation scenario for the United States is a very low risk.

Investment Implications

“But then finally the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against “real” goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap paper. Nobody wants to give away anything against them.” (Von Mises, 1949)

What’s described above by the late Ludwig Von Misses is what happened in Germany in the 1920s. This is the worst-case scenario. This is doom and gloom. I am certainly not predicting this in the United States. However, we must respect history.

Investors must not ignore inflation. Governments need inflation and abhor deflation. History tells us that financial assets tend to inflate along with the money supply. While the ideas below are not an exhaustive list, they are a good start in building a diversified portfolio. Investors should also consider their personal risk capacity, tolerance, and tax situation.

Investing in strong, global companies with low debt and pricing power remains a great strategy for investors. Many of these companies can compound growth year after year passing this on to investors through earnings growth and dividends. Shocks in the market are common, so investors should be prepared for bumps in the road. Holding some capital in cash and short-term bonds is also smart even in higher inflationary periods. Investors should consider gold as part of a portfolio to hedge against monetary inflation. Finally, prime residential real estate has performed well during higher inflationary periods and should continue to hold value.

As the sun rose on October 10th, many in our area breathed a sigh of relief as Hurricane Milton did not create as many problems as predicted. Certainly, those a little further north near Tampa were not so lucky. The same can be said for those affected by Hurricane Helene in North Carolina. Our prayers are going out to those folks and we hope the damage can be cleaned up soon and life can get back to normal.

References

- Montier, J. (2013). Hyperinflations, hysteria, and false memories. In GMO.com. https://www.gmo.com/americas/research-library/hyperinflations-hysteria-and-false-memories_whitepaper/

- Polleit, T. (2022). Inflation, High Inflation, Hyperinflation. In Mises Wire. https://mises.org/mises-wire/inflation-high-inflation-hyperinflation

- Kimmel, R. (2024). A Scenario Survey as Washington Drifts Toward a Reckoning. In DoubleLine Capital. https://doubleline.com/wp-content/uploads/Debt-Spiral-Briefing_Kimmel_July-2024.pdf

- Von Mises, L. (2010). Human Action [Print]. Ludwig von Mises Institute.

DISCLOSURES & INDEX DESCRIPTIONS