Courage in the Storm

Posted:October 26, 2022

Categories:

Paul Hancock, CFP® October 26, 2022

There are days and there are decades. Then, there are days when decades happen. I quickly realized upon waking up at 2 AM on September 28, 2022, that this was going to be one of those days. I had been closely monitoring the path of Hurricane Ian as it slowly moved south from Tampa back towards Southwest Florida. Having lived in Florida now for almost 10 years, I’ve tracked my fair share of storms. While I do not consider myself an expert having only lived through Hurricane Irma in 2017, this storm looked different. Our family hunkered down at home as the wind ripped through town for most of the day. As evening approached, we began getting reports about the damage, much of it focused on the awful storm surge that affected coastal areas. The fallout from Hurricane Ian has been devastating to many in our area and our hearts and prayers go out to those affected.

Financial markets have been experiencing their own kind of storm during the past year. Volatility has again picked up along with higher inflation and higher interest rates. The risk of a recession appears imminent in the United States.

Stock Markets

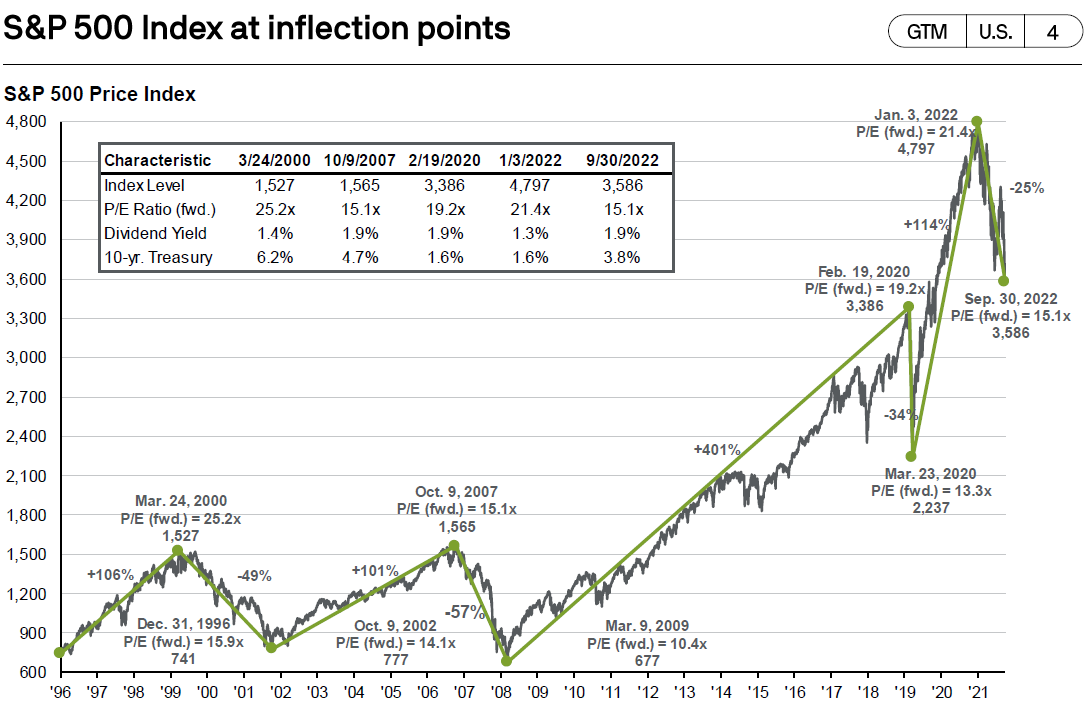

Bear markets are nothing new in stocks, although they have been much less common in the past decade. As seen below in figure 1, the S&P 500 has marched higher and higher since the Financial Crisis of 2008/2009. The markets even bounced back stronger post-COVID-induced downturn. Years of low interest rates, low inflation, and easy monetary policy have greatly benefited stock investors. Many of these policies have begun to reverse, directly affecting the direction of the market. Investing in the stock market requires patience. The longer your time horizon, the better. Even those in retirement can potentially have long time horizons.

Investors should not fear bear markets. Rather, bear markets should be thought of as a chance to add money to depressed assets. Buying when fear is high is part of being patient. For many investors, that means continuing to dollar cost average month after month. For others, that means holding strong to current positions while looking to reallocate to cheaper areas of the global stock market.

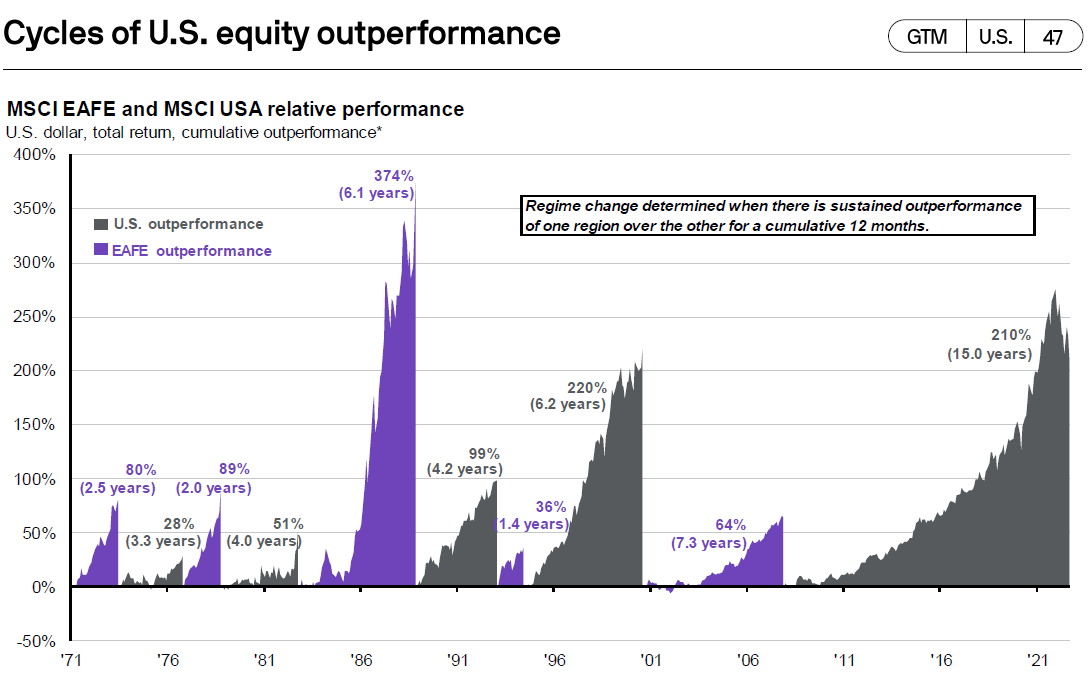

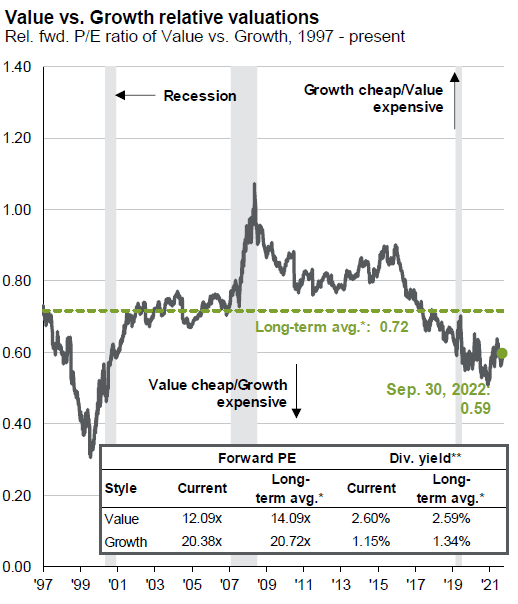

As seen in figure 2 below, stock markets in the US have dominated their foreign counterparts. This is also true for large cap growth stocks vs. value stocks (figure 3). Markets can certainly stay overvalued for long periods of time and thus exhibit strong momentum. However, shifting portfolios to cheaper assets can prove valuable as markets change. International stocks, both in Europe and Emerging Markets continue to look attractive relative to US stocks. This is especially true within value stocks.

Figure 1: S&P 500 Index at inflection points

Source: JP Morgan

Figure 2: Cycles of U.S. equity outperformance

Source: JP Morgan

Figure 3: Value vs. Growth

Source: JP Morgan

Bond Markets

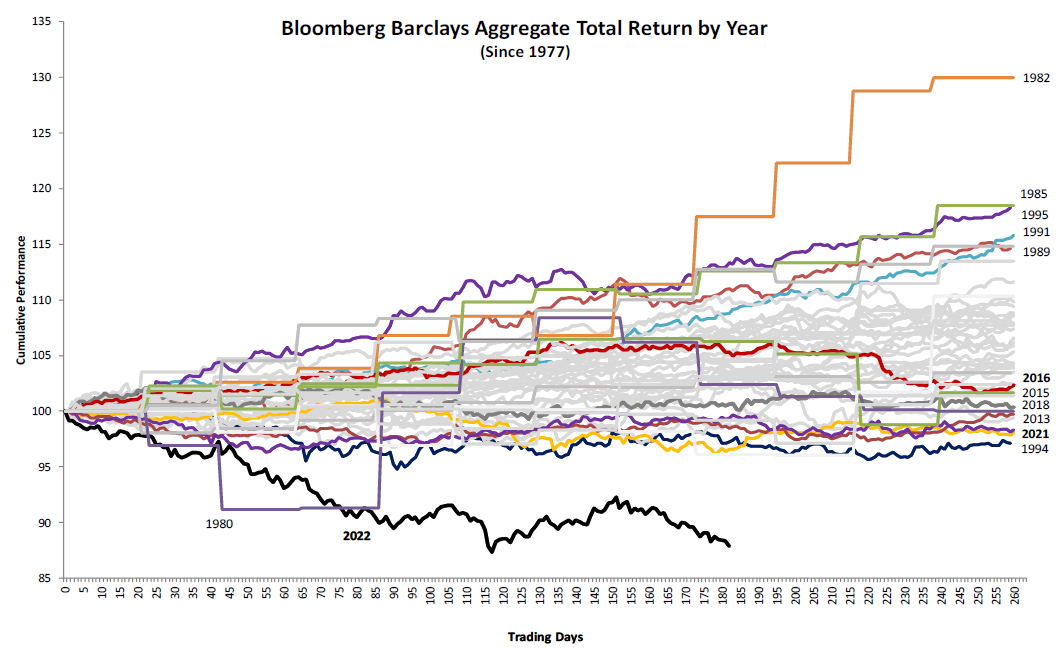

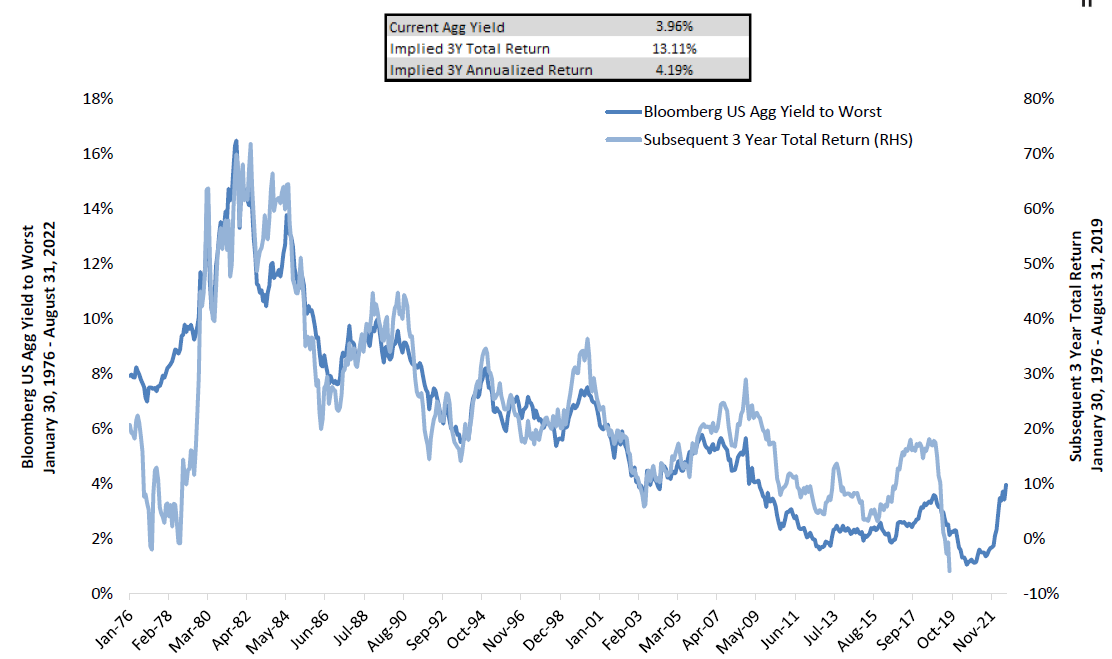

The once bulletproof bond market has been battered in 2022 as interest rates have increased dramatically along with inflation. Bonds with longer durations have dropped more in price than those with shorter durations. The Barclays Aggregate Bond Index has seen its worst decline since 1977 as seen in figure 4 below. However, the upside to depressed bond prices is, of course, higher interest rates! As seen in figure 5 below, future-looking returns from the bond market look much more attractive than in recent history. Evidence of this can easily be seen in what you can earn through short-term instruments such as high-yield savings accounts, short-term CDs, and even short-term US treasury bills. Much likes stocks, investors need to hang in and not panic with the bond portion of their portfolio. Those utilizing individual bonds in portfolios should hold steady with current positions and welcome new purchases at higher interest rates. Those holding bonds through funds or ETFs should also hold steady and allow managers to buy new bonds at higher interest rates.

Figure 4: Bloomberg U.S. Aggregate Bond Index Performance (as of 9/13/2022)

Source: DoubleLine

Figure 5: U.S. Aggregate Yield and Forward Returns

Source: DoubleLine

References

- JP Morgan Guide to the Markets ® U.S. / 4Q 2022

- DoubleLine Webcast/Slides from 9/15/2022

DISCLOSURES & INDEX DESCRIPTIONS